Hey there,

I'm Dan, founder of Quote.com. We've helped people find the best prices on insurance for over 5 years.

Picking out insurance can seem overwhelming. Between the jargon, the complicated policies, and the fine print, it's hard to know what a plan covers and how much it really costs.

That's why we put together this cheat sheet and checklist. While there's so much to know, this list can serve as a starting point for researching what type of plan you need including tips for getting the best deal.

You don't have to read over every section. Just look at the type of insurance you're interested in and then click on any of the linked resources for a more in-depth dive into that topic.

Thanks for visiting Quote.com. I hope learning more about what insurance you need helps.

Dan

There are six types of insurance to consider investing in:

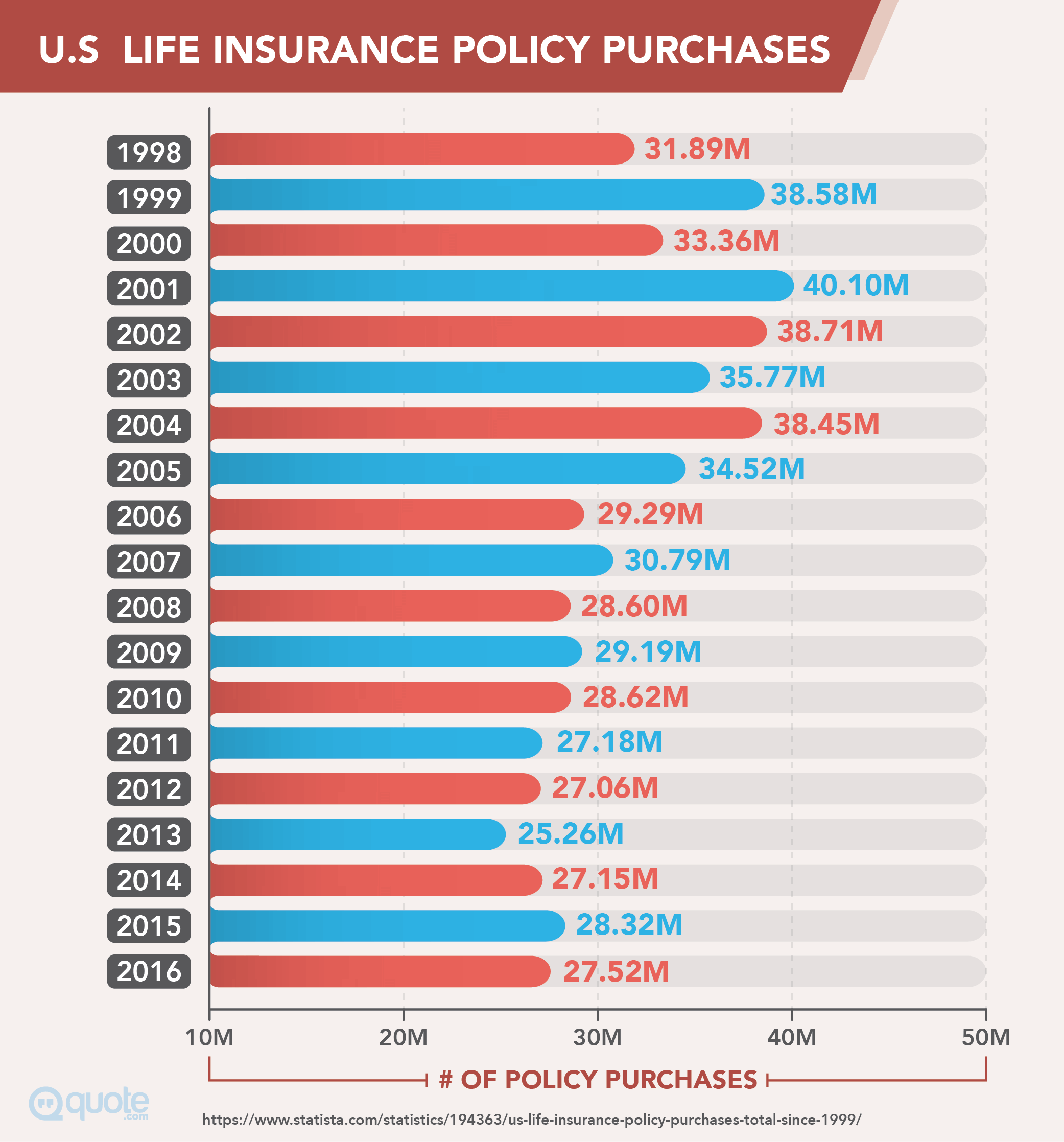

Life insurance will protect your family's financial future

Life insurance keeps your spouse, partner, or children from facing financial hardships in case the worst should happen. This can protect your family from expensive funeral costs and provide for them for years after you're gone.

I went with a higher life insurance plan because I want to make sure my wife and kids can afford to stay in our home and maintain the business for a longer period of time without having to worry about paying the bills.

It's not just a salary that goes away with a loved one when they die. Its security. Its knowing you can pay the bills every month while you contemplate a new normal.

I want my family to know the last thing they will have to worry about is whether they can pay our monthly bills while dealing with losing a husband and father.

Gain peace of mind by picking the right plan.

Your life insurance coverage needs will change over time.

If you're young and just starting a family, you need a greater amount of coverage. Your long-term insurance plan should enable your loved ones to cover expenses like mortgages or other bills and help them save for retirement or college without your supporting income.

When you're on better financial footing later in life, you can use your life insurance policy as an investment vehicle much like a 401(K). That's because certain types of policies let you contribute pre-tax income and save when tax season rolls around.

After you've retired, you may no longer need long-term life insurance coverage depending on how much you saved during your working years.

The most important things you should know about life insurance

Life insurance comes in two broad categories:

Term life insurance. This plan covers a person for a fixed period of time, during which you pay a fixed annual or monthly premium. It pays out a benefit if you pass away during this time period.

Whole life insurance. This plan doesn't have a set time period and is effective as long as you pay your policy's premiums. It's more expensive but accumulates a cash value that grows over time.

The top ten life insurance tips

Get enough coverage. Your policy should pay out enough to cover 15 years worth of your income. That means if you make $50,000 per year, get a policy worth $750,000.

Term life insurance is most likely enough. Only choose whole life if you're looking for an investment vehicle or way to shave a few dollars off your taxes.

Don't let your coverage lapse. Missing a premium payment may make your term life insurance null and void. That means you have to get a new policy, which can come with a large increase in premiums if you're significantly older than when you first got the policy.

Stop smoking. The best (albeit not easiest) way of lowering your premiums is to quit cigarettes.

Buy it early. The younger you are when you purchase a policy the cheaper it will be.

Drive safe. Your driving record affects your premiums so keeping a clean record saves you money.

Pay annual premiums. Most insurers will cut you a discount if you pay your premiums on a yearly basis instead of monthly.

Ask about price breaks. Some insurers will cut your rates if you reach certain coverage amounts. That means you could potentially save by getting a $250,000 policy instead of a $240,000 policy.

Be upfront about pre-existing conditions. Not stating these could lead to your policy getting suspended down the road, or prevent benefits from getting paid out to your beneficiaries.

You can still get life insurance with a pre-existing condition. Certain types of life insurance like a simplified issue or guaranteed issue policies are less stringent about who they accept.

When not to get life insurance

If you don't have any dependents or spouses, you don't need life insurance.

The best life insurance resources

Auto insurance protects your car and pocket

There's one simple reason you should get auto insurance: It's the law. You legally can't drive without the state-mandated minimum amount of insurance.

Auto insurance can also keep you from getting sued if you're at fault in an accident, as well as pay for damages to your vehicle.

Know which kind of auto insurance is right for your vehicle

Everyone will need at least the state-mandated minimum in order to be on the road. If you're strapped for cash, this may be all you should get for right now.

If you own a new car or a more expensive vehicle, you should consider additional coverage. Consider comprehensive, collision, or gap insurance.

Folks driving a motorcycle or classic car should also consider specialty products that cater to their needs.

One thing our financial advisers suggested was having an auto insurance policy that could cover for almost any accident imaginable simply because we drive higher end vehicles.

The assumption is, if you drive, for example, a new Cadillac, you must have money- right? While that might be true, you don't want the person you were in an accident with to automatically assume they hit the jackpot when you hit them!

Having a higher auto insurance policy might just protect you from a personal lawsuit above and beyond what your insurance policy would pay out, in the event you are in a serious accident.

How life auto insurance fits into your finances

Car accidents can be financially devastating. If you're not insured, you could end up paying thousands of dollars for a new vehicle.

More than that, you could face a lawsuit if you're at fault for an accident and don't carry enough insurance.

Remember, cheap car insurance premiums won't save you money if your policy doesn't provide the protection you need.

The most important things you should know about auto insurance

Different types of car insurance pay out in different situations.

Liability insurance. This policykicks in if you're at fault in an accident. It doesn't cover you or your vehicle but instead, pays up to a certain limit for property damage and medical bills for other people involved in a wreck.

Collision insurance. This policypays for your car if you're at fault in an accident.

Comprehensive insurance. This policy will cover your car if it's damaged by some types of inclement weather, or if it's vandalized or stolen.

The top ten auto insurance tips

Safer car, lower premiums. Many auto insurers will slash rates if your car has an alarm system, anti-lock brakes, or other features that make it harder to steal or safer in a wreck.

Do a cost/benefit analysis for collision and comprehensive insurance. Think about how much your car is worth before getting collision or comprehensive coverage. If you pay $1,000 per year for collision insurance on a $3,000 car, after three years you'll pay more than your car is worth.

Get gap insurance for new cars. Some insurance policies only pay out a vehicle's current value after a wreck rather than what you paid for it, meaning you could still be making payments on a car sitting in a junkyard. Gap insurance keeps this situation from happening by paying out the original price of the car.

Consider usage-based insurance. Letting your insurer track when and how you drive can lower your rates – as long as you're a safe driver.

For lower rates, raise your deductible. You pay a little more in case of an accident, but this can save you money over time.

Get good grades for cheaper insurance. Some insurers offer lower rates for college and high school students making at least a B average or above.

Life happens. Certain life events like switching careers, getting married and buying a house can lower your premiums. Inform your insurer if any of these happen.

Take a defensive driving course. These courses can do more than prevent your rates from increasing after a speeding ticket. Taking them with a clean record can slash your premiums.

Switch cars. Insurers charge higher rates for certain vehicles. If you really want a lower rate, swap out the sports car for a minivan.

Drive less. Most insurers offer a low-mileage discount for people who drive 5,000 miles or less per year.

When you shouldn't get auto insurance

If you don't drive or own a car, you don't need auto insurance.

The best auto insurance resources

Health insurance keeps your body and wallet healthy

Health insurance is probably the most important type of insurance you'll ever get. Other types of insurance can cover your home, car, or trip, but your health is more valuable than all of those items put together.

Medical bills can be incredibly expensive. With health insurance, getting a major surgery or treatment for a serious illness won't put you in dire financial straits.

It does not have to be a major medical illness or planned medical expenses due to a pregnancy. My wife woke up in the middle of the night in excruciating pain, and literally begged me to take her to the ER immediately. (This is the same woman who was up showering less than six hours after a c-section with our daughter- she has a crazy high pain tolerance!)

When we got to the ER, the initial diagnosis was either a ruptured ovarian cyst, or appendicitis. Sure enough, her appendix was about to rupture, and she was rushed to emergency surgery.

Without a solid insurance plan, this unavoidable, middle of the night health surprise would have cost us over $40,000. With insurance, we spent about $2,000 out of pocket.

How to pick the right health insurance plan for you

This will vary wildly, and only keep changing depending on how healthcare laws and regulations change. For now, consider these options.

Employer-provided health insurance. This plan is often a good option if it's available through your employer. Most of these plans are affordable and offer decent benefits.

Bronze, Silver, Gold, and Platinum health insurance. These plans offered through exchange on HealthCare.gov pay between 60-90% of most medical costs. Higher levels of coverage mean higher premiums though, so consider which one is right for your financial situation.

Catastrophic plans. These plans are only available to those under 30 years old but have the lowest premiums. If you're young, don't go to the doctor often, and are in good health, this may be a decent option.

The most important things to know about health insurance

Health insurance terminology can make picking a plan more daunting than it really is. Here's how to speak your health plan's language:

Premiums. This is how much you pay every month for health insurance.

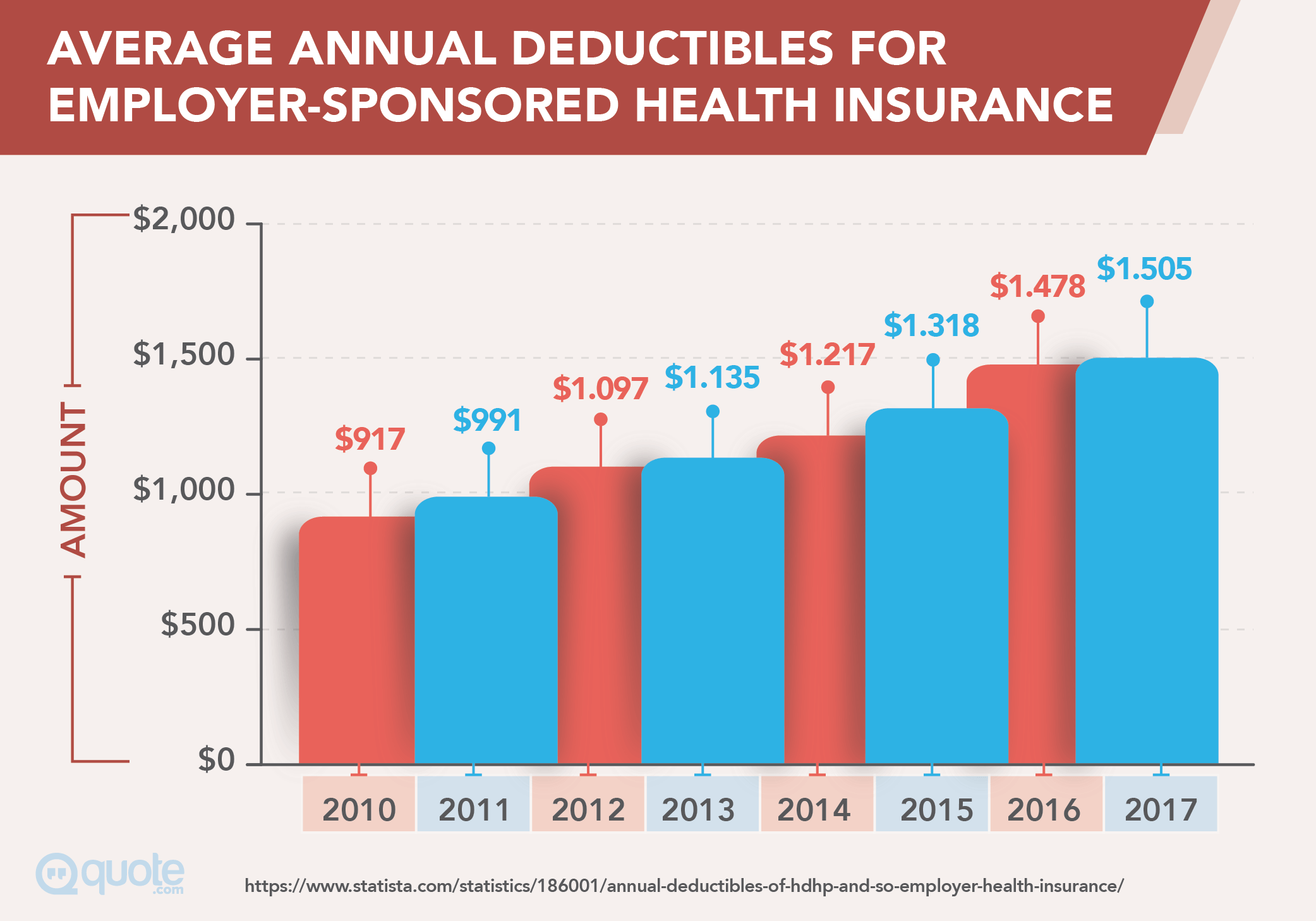

Deductibles. This is how much you have to pay before your health insurance kicks in. Different types of costs like prescriptions may have their own deductible that needs to be met.

Copays. You pay this flat fee when you visit the doctor.

Coinsurance. This is the percentage of the charge you pay for care.

In-network. These health care providers have contracts with your insurance company to give plan members discounted rates.

Out-of-network. These providers don't have such contracts, so you pay more for visiting them.

Enrollment period. This critical time is when you can sign up for plans through government or state healthcare exchanges.

The top ten health insurance tips

-

Different states have different special enrollment periods.

That means you can sign up for insurance outside of the usual enrollment period. If you need insurance now, check whether you qualify for one of these.

-

Watch your savings.

Plans purchased on the healthcare exchange offer special tax subsidies, but these vanish under certain conditions like becoming eligible for employer-offered health insurance. Consider that before you decide on keeping a plan purchased on the exchange over one offered by your work.

-

Stay healthy.

Preventative care is covered under most insurance plans. Keeping yourself healthy by using these services keeps your premiums low.

-

Report your income.

Healthcare exchange premium tax credits change based on your income. Make sure to report any increase or decrease in your earnings to maximize savings, or to prepare for a larger bill.

-

Consider a Health Savings Account

. These let you contribute pre-tax income to save for any health expenses. That means you can be better prepared for an unexpected doctor's visit and pay less to the IRS.

-

Ask for outside help.

Treatment for some conditions or diseases may result in charges that go beyond what your health insurance can cover. Ask your doctor about any organizations that offer assistance with payments.

-

Get your steps in.

A few insurance plans offer discounts for using Fitbits or similar devices. Check if you qualify for these savings.

-

Prescription discounts.

Pharmaceutical manufacturers often offer discounts on medication for people in certain income brackets. If your plan doesn't offer adequate prescription drug insurance coverage, check whether the maker or your medication offers these savings.

-

Freelancer tax deductions.

If you're a freelancer, you can get a tax deduction for the cost of your health insurance deductible. Speak with an accountant to see if you can take advantage of this.

-

Consider your options.

If both you and your spouse qualify for employer-provided plans, check whether one of them makes better sense for your coverage needs and financial situation.

When you shouldn't get health insurance

Quite frankly, you always need health insurance. Without it, you risk the double whammy of suffering bad health and the financial consequences of that bad health.

The best healthcare insurance resources

Home insurance shores up the roof over your head

Your home is your biggest investment. Home insurance keeps all that money from vanishing as a result of one bad accident.

Next to health insurance, home insurance is one of the most important policies you can own. Without it, you could lose tens or hundreds of thousands of dollars if something happens to your house.

Recently, we had a huge palm tree crack our pool deck, the side of the pool, and a portion of the foundation of our home. The tree was amazing- and the cracking happened literally within a week. We had no idea this beautiful tree was one storm away from coming down onto our roof!

While trying to figure out how to fix all the problems the tree caused, we discovered our home owners insurance would not cover tree/root damage unless the tree actually came down onto our home and damaged our home significantly.

We never considered whether the policy we had would need to include coverage for tree root damage, and found out most policies do not cover this.

The worst part for us was having no choice but to spend a ridiculous amount of money out of pocket to remove the tree, make repairs to the deck, pool, and home foundation, and also remove another smaller palm tree which was going to cause issues if we did not remove it too.

Moral of my story this time is to make sure you have the coverage you need, for any possible scenario you can get coverage for that would apply to your specific property.

Get the home insurance coverage you need

Most home insurance plans cover three basic areas:

Dwelling coverage. This planprotects the actual structure of the house itself.

Contents coverage. This plancovers the items in your house.

Personal liability coverage. This plan pays for medical bills if someone gets injured inside your house.

These types of coverage should be where your home insurance search starts, not where it ends.

Depending on your situation you may need additional types of insurance protecting against floods, earthquakes, or other dangers.

The most important things to know about home insurance

Some home insurance policies will only pay out the value of your home at the time it was appraised. That means a home insurance policy may not be enough to fully cover rebuilding or repairing your home if it doesn't have one of two essential forms of coverage.

Extended replacement coverage.It's important to note that payouts cap out at 125% of your home's insured value.

Inflation guard. This perkmakes sure your home's insured value stays current with its current worth on the marketplace.

The top ten home insurance tips

-

Fix it yourself it for lower premiums.

If you can, repair anything yourself or hire a contractor to fix damages that cost under $1,000. Filing multiple claims can increase your premiums.

-

Find out if you need flood insurance.

You're legally required to get this if you live in a floodplain.

-

Insure your valuables.

If you have expensive art, jewelry or antiques in your home, get a separate policy for these items. That way, replacing them doesn't eat up most of your policy's payout.

-

Get an independent walk-through.

Ask a homebuilder to quote you how much your home is worth to accurately determine how much insurance you need.

-

Get replacement cost instead of actual cash value.

Actual cash value covers the full cost of replacement for your items.

-

Safety first.

Installing smoke alarms or security systems will lower your premiums.

-

Plan for the future with ordinance or law insurance.

If you plan on living in your home for a few decades, these types of insurance will cover any charges required to bring your house into compliance with future building codes.

-

Get external structures their own policies.

Otherwise, your gazebos, detached garages, or sheds may not be covered under your home insurance policy.

-

Bundle up.

Many insurance plans will cut your premiums if you bundle your home and auto insurance together.

-

Insurance for the sharing economy.

Most plans won't cover any damages resulting from renting your home out on Airbnb or a similar service. Check whether your insurer offers special plans for these situations.

When is home insurance not right for you?

If you don't own a home, you don't need it.

The best home insurance resources

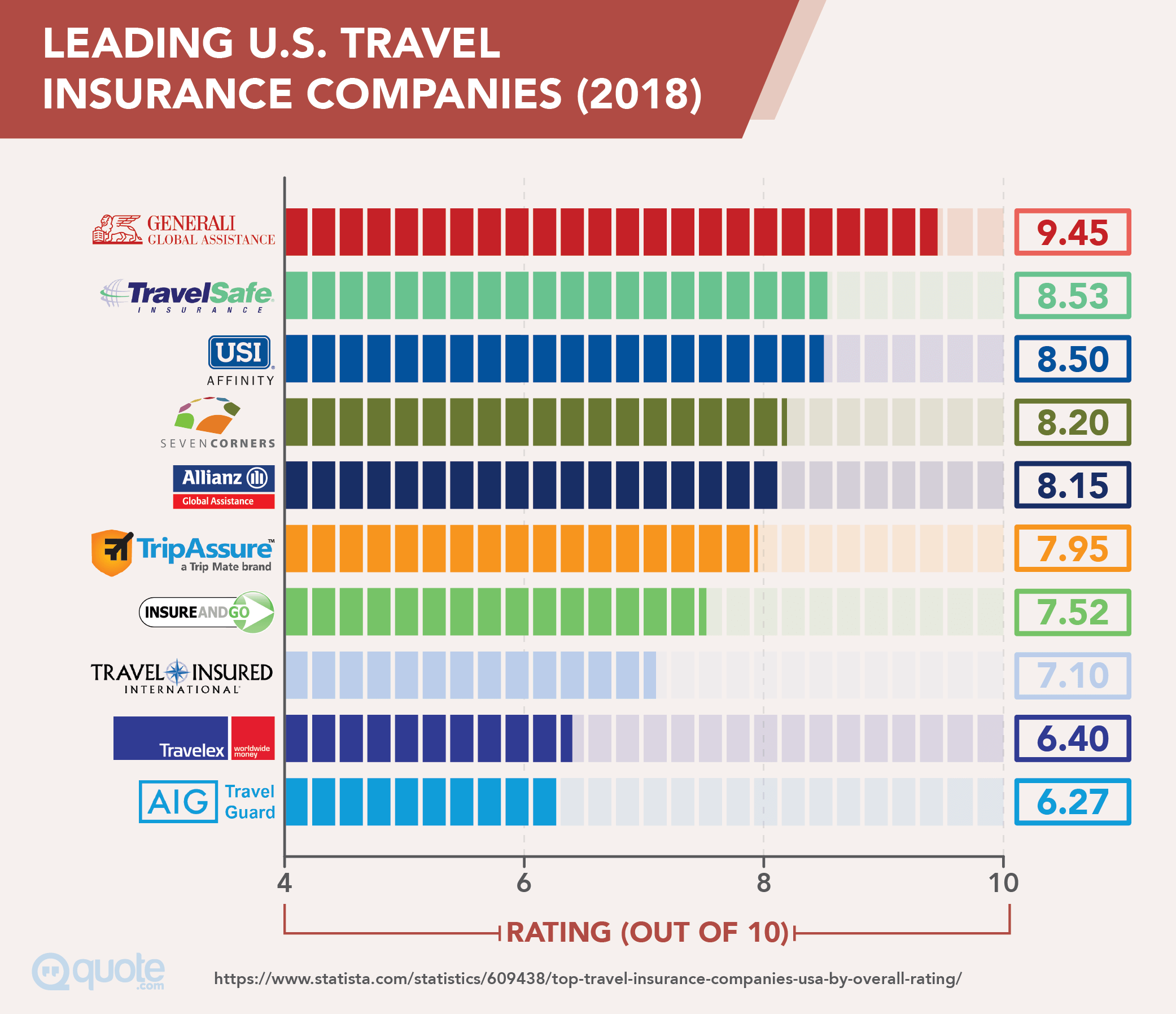

Travel insurance makes your trips extra relaxing

Vacation, cruises, and trips can cost thousands of dollars and that money can disappear if you have to cancel them at the last minute.

More than that, you can rack up jaw-dropping hospital bills if your health insurance doesn't cover medical care in a foreign country.

If you're planning a globe-trotting vacation, then it's worth spending a few extra dollars to make sure that you don't end up losing all that cash if you can't go.

The right kind of travel insurance can help you avoid these worst-case scenarios.

The best example here is cruises. We love to take cruises. But, every time we purchase our floating vacations, we opt for the travel insurance just in case one of us has a medical emergency and has to be helicopter evacuated off the ship or island.

After we saw an older man being evacuated after a cardiac related health issue, it was enough for me to invest the few extra dollars for the coverage.

And, when we had one of our cruises cancelled due to a hurricane, having the travel insurance gave us the option of getting a full refund or rebooking our trip on a different route.

Pick the perfect travel insurance plan for your vacation

Depending on the kind of trip you're taking, consider one of these forms of travel insurance:

Travel medical insurance. This plan covers medical treatment in a foreign country.

Evacuation insurance. This plan pays for getting you to the nearest hospital or back home in case of a medical emergency.

Cancellation insurance. This plan will cover the cost of your trip if you can't go on it.

Package travel insurance. This plan combines all of the above types of coverage into one easy plan.

The most important things to know about travel insurance

Your travel insurance will only kick in under certain conditions, so make sure you read your policy closely. For instance, most cancellation insurance plans will only cover your trip if the following prevents you from going:

- Sudden business conflicts

- Changing your mind

- Delays in processing your visa or passport

- An illness or injury

- Weather-related issues

Some policies won't protect you if your trip gets canceled due to an accident on the way to the airport, jury duty, or a fire or flood in your house. Make sure you do your research when picking out the right policy.

The top ten travel insurance tips

-

You may already be covered.

Your credit card, health insurance, and car insurance may offer some of the same protections provided by travel insurance. Check them before taking out a policy.

-

Shop around.

Don't buy your policies directly from travel agents because they may be selling the policy that will net them the highest sales commission.

-

Special insurance for adventurers.

If you're planning on scuba diving, skiing, spelunking or skydiving on your vacation, most basic travel insurance plans won't cover injuries resulting from these activities. See if you need to upgrade your coverage to get protected.

-

Use the Free Look Period.

Every travel policy comes with a 10-15 day Free Look Period when you can review, change, or cancel your coverage based on your needs.

-

Primary coverage.

Look for travel insurance plans that act as primary coverage. They'll kick in before your other forms of insurance and save you from out-of-pocket expenses.

-

Make sure your carrier is covered.

Not all airline carriers and tour operators are covered under travel insurance policies. Make sure yours is before buying a policy.

-

Medicare doesn't cover you overseas.

If this is your primary health insurance, get travel medical coverage.

-

You may not need baggage insurance.

If you check your bags, they're covered by the airline in most cases.

-

When you need rental car insurance.

During domestic trips, your regular car insurance will cover you in the United States. If you're planning on renting a car abroad, you can get it covered under your travel insurance.

-

Get it fast.

Getting your travel insurance as soon as possible gives you the most amount of time to cancel in case you're prevented from going on your trip.

When is travel insurance not right for you?

If you're not planning on traveling, you don't need this type of insurance. It's also not necessary if you're going on a low-cost trip.

The best travel insurance resources

Pet insurance keeps your furry feathered friends protected

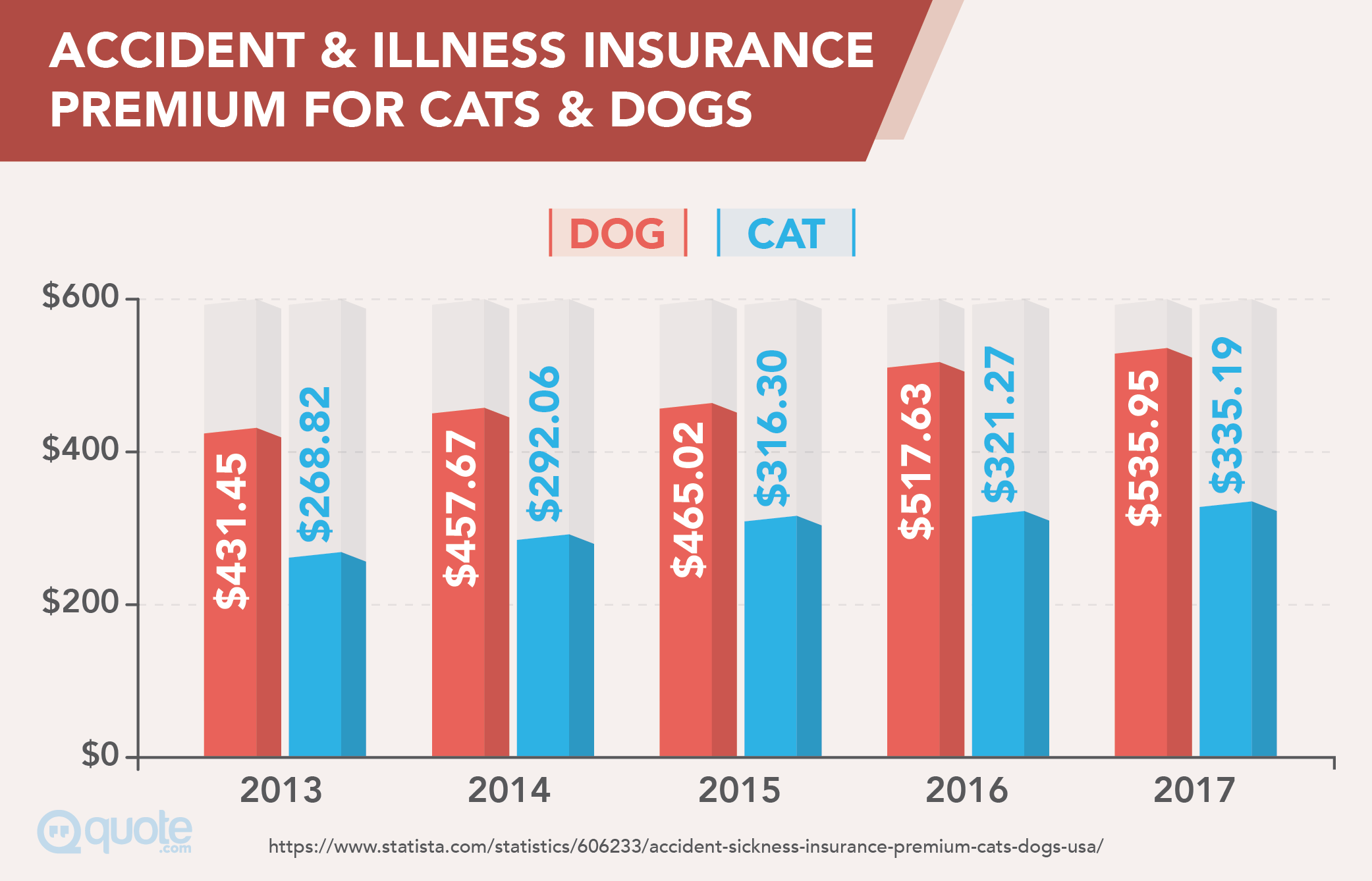

Medical bills for pets can now range into the thousands of dollars. If you want to get your animal companions the best medical care possible, you'll need pet insurance.

For most pet owners, pet insurance can seem unnecessary if they have a healthy animal. However, it can keep you from having to dig into your savings to cover a $1,000 vet bill if your pet gets injured or becomes ill.

A relative of mine had the most beautiful dog. She was super sweet, and was their "first kid." When she was about eight years old, she was diagnosed with cancer. My relatives were absolutely devastated.

The costs for treatment were simply beyond their means, but they could not bear the thought of not doing what they had to do for their baby. After a few treatments, she perked up and was doing better, but my relatives were in a very compromised financial position.

Their dog recovered quickly and lived another six years happily, but for my relatives, the bills are still present to this day. Had they had pet insurance, they would not still be dealing with the financial burden of doing what was best for their four legged friend.

How to pick the right pet insurance

You want a plan that will cover injury and illnesses. Don't think about pet insurance as a way of defraying costs for routine trips to the vet – it's for emergencies only.

The most important things to know about pet insurance

Pet insurance doesn't work like human health insurance. Instead of kicking in right when you pay your vet bill, you file a claim and the insurance company reimburses you later.

The deductibles work differently as well, falling into one of three categories:

Annual. The insurance pays out for the rest of the year once you've reached your deductible.

Per condition. Each condition has a deductible after which the insurance kicks in.

Per visit. You have to reach your deductible each time you take your pet in for treatment.

The top ten tips for pet insurance

-

Purebreds beware.

Some pet insurers don't cover diseases and conditions genetically linked with certain breeds of pets. Read your policy carefully.

-

Pets can have pre-existing conditions too.

That may exempt them from being covered by pet insurance.

-

Young pets are cheaper to insure.

Insuring your puppy or kitty keeps premiums low and means they can get the best care in case they swallow something harmful or injure themselves playing.

-

Don't buy pet wellness coverage.

This covers vaccines and typical trips to the vet. However, it usually costs more overall than the visits.

-

Think about liability insurance.

If you have a particularly rambunctious animal, this could protect you from paying out money as a result of a lawsuit.

-

Watch out for waiting periods.

Some plans delay their insurance coverage for a certain amount of time after you purchase a policy, which could put you at risk of high vet bills.

-

Always choose the highest deductible you can afford.

Pet insurance is for emergencies so you want a high deductible and low premium.

-

Watch out for capped payouts.

Some plans cap how much they'll cover, which can lead to a nasty surprise when filing a claim.

-

Create a pet emergency fund.

If you can't afford pet insurance, set aside whatever you can to pay for any unexpected pet medical bills.

-

Get a multi-pet discount.

Some insurers reduce your rates if you insure more than one animal through them.

When you don't need pet insurance

People without pets need not apply.

The best pet insurance resources

What insurance do you need?

Any insurance tips that have saved you money or more?

Have you found a workaround getting a type of insurance?

I'd love to know how many others out there have had similar experiences or perhaps similar experiences with very different outcomes! Please leave a comment below.